Caps And Floors Ppt

Options Caps Floors

Concrete Wall In Empty Room For Artwork 3d Rendering Stock Photo Aff Empty Room Concrete Wall Stock In 2020 Concrete Wall Concrete Empty Room

Ppt Caps Floors And Collars Powerpoint Presentation Free Download Id 6803699

Options Caps Floors

Ppt Interest Rate Caps And Floors Vaulation Guide Powerpoint Presentation Id 7898141

Interest Rate Swaps Caps

Caps and floors are typically traded on 3 months simple spot rates in the us market and on 6 months simple spot rates in the euro market.

Caps and floors ppt. The bondholder effectively sold an option to the bond issuer. An interest rate cap is a derivative in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price an example of a cap would be an agreement to receive a payment for each month the libor rate exceeds 2 5. These option products can be used to establish maximum cap or minimum floor rates or a combination of the two which is referred to as a collar structure. They are most frequently taken out for periods of between 2 and 5 years although this can vary considerably.

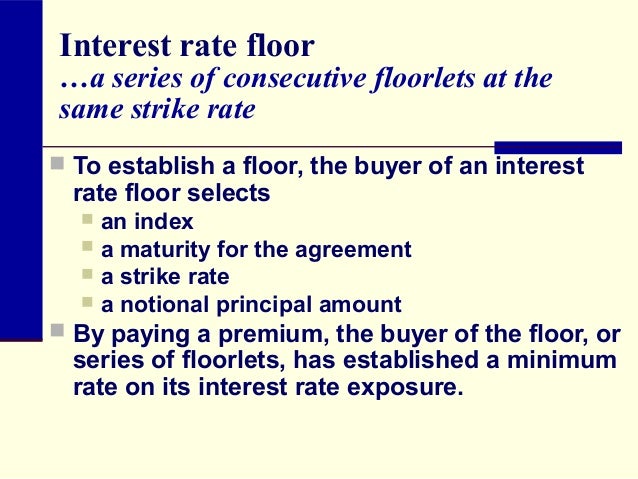

An interest rate floor is an agreed upon rate in the lower range of rates associated with a floating rate loan product. Caps restriction on the maximum coupon rate cap. Coupon rate taken to be max rfloat rfloor. We see that maturities range up to 30 years.

Coupon rate taken to be min rfloat rcap. Floors minimum coupon rate specified for a floating rate security floor. The first column gives us the cap prices in percentage points. Capped floater floater minus cap.

A price floor is the lowest legal price that can be paid in markets for goods and services labor or financial capital. Interest rate floors are utilized in derivative. Caps floors and collars 3 capped floater consider the net position of the issuer of 100 par of a floating rate note who either buys a matching cap from a dealer or else embeds the cap in the note at issue. Perhaps the best known example of a price floor is the minimum wage which is based on the normative view that someone working full time ought to be able to afford a basic standard of living.

Interest rate caps floors and collars are option based interest rate risk management products. As long as the interest rate remains within the strikes the trader has paid a premium and makes a loss. Figure 7 15 payoff of bought cap and floor. This would be the case for example in a mortgage contract which limits the variability of the floating rate from 0 to 3 for instance.

These products are used by investors and borrowers alike to hedge against adverse interest. The bond issuer sold an option to the bond holder. But if the interest rate moves beyond the strikes on either side the trader gains if the gross payoff more than compensates the premium paid which cumulates the premium of the cap and of the floor.

Screen Shot 2015 06 08 At 2 17 47 Pm Diy Flooring Diy Wood Floors Unique Flooring

Download Old Wooden Floor For Free In 2020 Wooden Planks White Wood Texture Wooden Flooring

Pin By Ryan Mitchell On New Home Ideas Rustic House House Styles Wood

Awesome Flooring Rustic House House Styles Wood

Dance Floor Mix 14 Ad Sponsored Ad Mix Dance Floor In 2020 Dance Floor Flooring Dance

Mail Kristin Croucher Outlook Family Room Home Decor Side Table

Interest Rate Caps And Floors Vaulation Alan White Finpricing Ppt Download

Cordwood Floors Cordwood Homes House Flooring End Grain Flooring

Grillworks Inc Floor Outlets Floor Outlet Cover Highland Homes

Flooring Unique Flooring Flooring Log Homes

Caps And Floors Interest Rate Derivatives Coursera

Bodensteckdose Bs8802 B 1xschuko 2xrj45 Bs8802 B Rj45 1 Jpg 2560 1600 Flooring Wood Floors Floor Outlets

Sovereign Lakeview Is A Upcoming Luxurious Apartment Project Which Is Located At Vidrayanapura Bda Layout And Jalahalli Lake View Sovereign Apartment Projects